A simple strategy that cuts the cost of waiting in half — especially if you still have a mortgage.

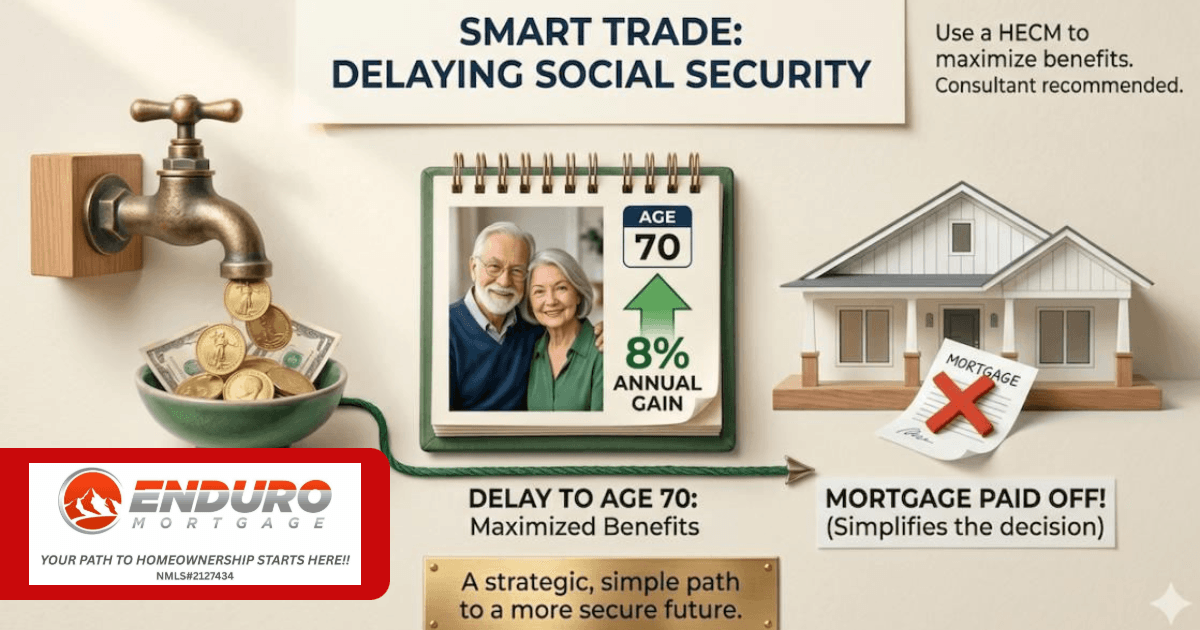

Most people want to delay Social Security because the benefit grows 8% per year. The challenge is covering the income gap while you wait.

Here’s the surprising part:

If you still have a mortgage, delaying Social Security is much cheaper than you think.

Use a reverse mortgage line of credit (HECM) to cover the income gap.

You’re paying about 6% interest… to get an 8% guaranteed increase in your Social Security.

Using the HECM instead of your IRA avoids a big tax hit and keeps your retirement savings working for you.

3. The Big Surprise (Most People Miss This)

3. The Big Surprise (Most People Miss This)If you still have a mortgage, the reverse mortgage pays it off automatically.

Let’s use simple numbers:

You need $8,000/month

You get $2,000/month from a pension

Your mortgage payment is $3,000/month

Before the reverse mortgage, your “gap” is:

$6,000/month

But once the reverse mortgage pays off your mortgage, that $3,000 payment disappears.

$3,000/month not $6,000.

You just cut the cost of delaying Social Security in half.

The Bottom LineWith this strategy:

You get the full 8% Social Security increase

You avoid a big tax hit

You protect your retirement savings

And you cut the cost of waiting by 50%

Delaying Social Security doesn’t have to be stressful or expensive. Sometimes the smartest financial moves are the simplest ones.

Representing: Enduro Mortgage, Colorado Mortgage Company Registration

NMLS# 2127434 Regulated by the Division of Real Estate

EQUAL HOUSING OPPORTUNITY https://nmlsconsumeraccess.org