Most people see rising interest rates and inflation as the "villains" of their retirement story. They’re the things that shrink your bank account and make your portfolio sweat.

But what if you had an account where higher interest rates were actually a good thing?

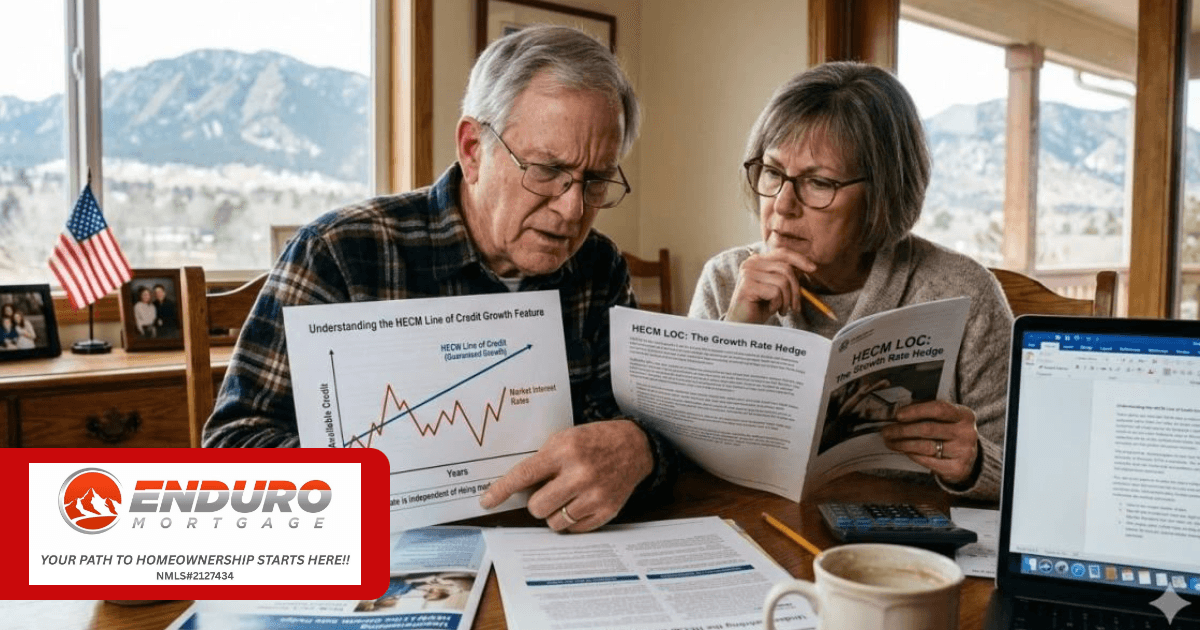

The "Wait... What?" Factor

It sounds backwards, but there is a specific type of credit line (an FHA-insured HECM) that behaves differently than any other loan on earth.

Here’s the part that makes people double-take: The unused portion of this line of credit grows at the same interest rate the loan itself charges.

· When inflation stays low, the line of credit grows steadily.

· When the Fed hikes rates to fight inflation, the growth rate on that available cash matches it.

Basically, at the exact moment your stocks are struggling, and your grocery bill is skyrocketing, this "bucket of backup cash" gets bigger, faster.

Why This Matters Right Now

Usually, when prices go up, retirees are forced to sell their investments at a loss just to pay the bills. That’s a recipe for running out of money too soon.

Instead of raiding the portfolio while it’s down, you just tap into this growing line of credit. It’s tax-free, it doesn't care what the S&P 500 is doing, and it’s been sitting right under your feet (literally, in your home equity) the whole time.

Let’s Stop Treating Home Equity Like a "Break Glass in Case of Emergency" Box

For years, we’ve been told to ignore home equity until things get desperate. That’s outdated thinking. In a world where inflation won’t quit, your home shouldn't just be a place to sleep—it should be the engine that protects your other investments.

Representing: Enduro Mortgage, Colorado Mortgage Company Registration

NMLS# 2127434 Regulated by the Division of Real Estate

EQUAL HOUSING OPPORTUNITY https://nmlsconsumeraccess.org