As a homeowner, you've likely built up significant equity in your property over the years. This valuable asset can be a source of financial flexibility, whether you need to cover unexpected expenses, fund a large project, or supplement your retirement income. Two common ways to access this equity are a reverse mortgage and a Home Equity Line of Credit (HELOC). While both use your home as collateral, they function in fundamentally different ways. Understanding these differences is crucial for making the right financial decision for your specific situation.

A HELOC is a revolving line of credit, similar to a credit card, that is secured by your home's equity. You are approved for a maximum credit limit and can draw money as needed during a set period, known as the draw period (typically 10 years). During this time, you often only have to make interest-only payments on the amount you've borrowed. Once the draw period ends, the repayment period begins, and you'll make payments that include both principal and interest.

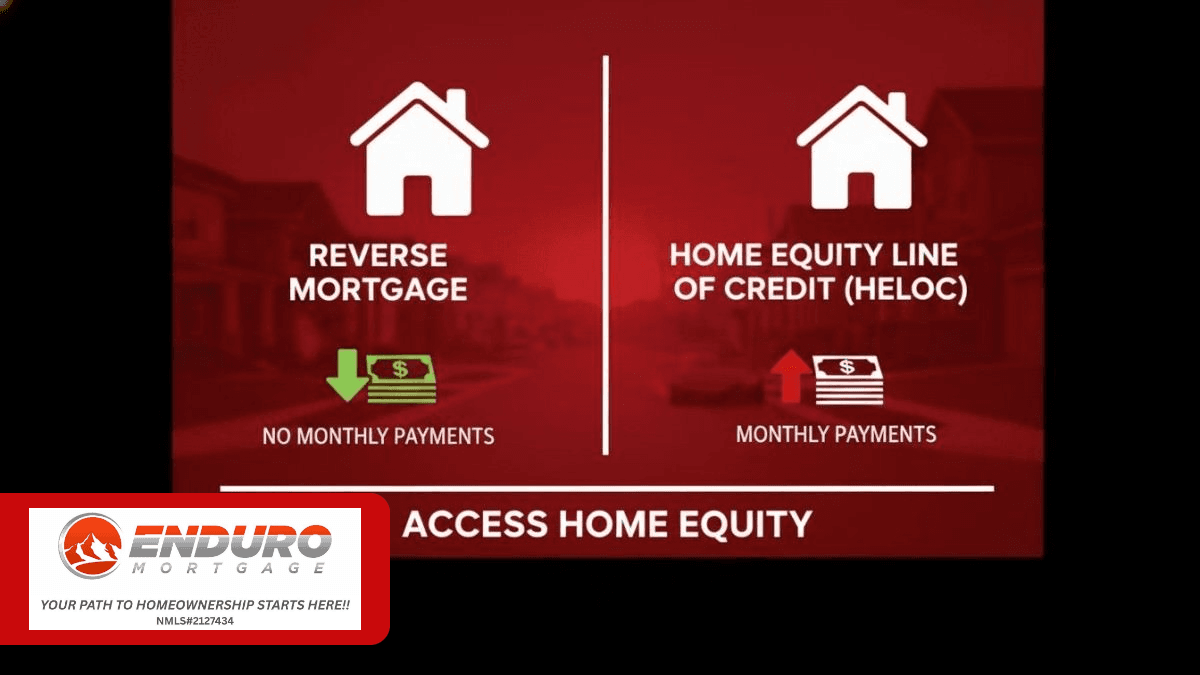

A reverse mortgage, on the other hand, is designed for older homeowners, typically those aged 62 or older. Unlike a traditional mortgage where you make payments to a lender, a reverse mortgage works in reverse: the lender pays you. You can receive the money as a lump sum, monthly payments, or a line of credit. A key feature is that you are not required to make monthly repayments on the loan as long as you continue to live in the home and meet the terms of the agreement, such as paying property taxes and insurance. The loan, plus accrued interest, becomes due when you sell the home, move out, or pass away.

| Feature | Reverse Mortgage | Home Equity Line of Credit (HELOC) |

| Eligibility | Must be 62 or older; must live in the home as your primary residence; must have a significant amount of equity. Credit score and income requirements are generally more lenient. | No age requirement; typically requires a good-to-excellent credit score, a low debt-to-income (DTI) ratio, and a stable income to demonstrate ability to repay. |

| Repayment | No monthly payments are required. The loan is typically repaid when the borrower dies, sells the home, or moves out. | Monthly payments are required, often interest-only during the initial draw period, and then principal and interest during the repayment period. |

| Disbursement | Can be received as a lump sum, regular monthly payments, a line of credit, or a combination. The amount you can borrow is based on your age, the home's value, and current interest rates. | Functions as a revolving line of credit. You can borrow what you need, when you need it, up to your approved limit. |

| Interest | Interest accrues on the loan balance, but you are not required to pay it monthly. The interest is added to the total amount owed, causing the loan balance to increase over time. | Interest is charged only on the amount you borrow. Rates are typically variable, meaning they can fluctuate based on market conditions, though some lenders offer a fixed-rate option. |

| Impact on Equity | Your home equity decreases over time as the loan balance grows. | Your home equity decreases as you borrow, but it can be rebuilt as you make payments. |

A reverse mortgage can be an excellent option for a senior who needs to supplement their retirement income but wants to avoid the burden of monthly loan payments. The funds are generally tax-free and won't affect Social Security or Medicare benefits. However, it's a significant financial commitment that can use up a large portion of your home's equity, potentially leaving less for your heirs. The upfront costs and fees are often higher than with a HELOC.

A HELOC offers more flexibility for a homeowner of any age who needs cash for various purposes, like home improvements, college tuition, or an emergency fund. The ability to draw funds as needed and only pay interest on what you use can be very beneficial. However, HELOCs require borrowers to meet stricter credit and income qualifications, and the variable interest rate can lead to unpredictable monthly payments. Failing to make payments on either a reverse mortgage or a HELOC can result in foreclosure, as your home is the collateral.

Choosing between a reverse mortgage and a HELOC comes down to your individual financial situation and goals.

Consider a reverse mortgage if: you are 62 or older, plan to stay in your home for the long term, and need to access cash without the obligation of a monthly payment.

Consider a HELOC if: you are willing and able to make monthly payments, have strong credit and a steady income, and want a flexible way to borrow for large, occasional expenses.

Before making a final decision, it's highly recommended to consult with a financial advisor and, for a reverse mortgage, a HUD-approved counselor to fully understand the implications and find the best fit for your needs.

Representing: Enduro Mortgage, Colorado Mortgage Company Registration

NMLS# 2127434 Regulated by the Division of Real Estate

EQUAL HOUSING OPPORTUNITY https://nmlsconsumeraccess.org